Gain the expertise to help clients navigate the financial, emotional, and practical realities of aging and strengthen your role as their most trusted advisor.

Now co-marketed with the Financial Planning Association.

Aging not only impacts those who are getting older, but also has an impact on those families and caregivers who want to ensure their loved ones are properly taken care of,” said 2023 FPA President James Lee, CFP®, CRPC®, AIF®. “Financial planners are in a unique position to provide empathetic support and guidance, but that means they need to understand the many issues older Americans face. Annalee and Bob are well-known experts in this space who have developed a program we are now delighted to offer through FPA for our members. A program we believe will best position our members and their clients for addressing these challenges with care and diligence

Why This Matters

Why Elder Planning Is No Longer Optional.

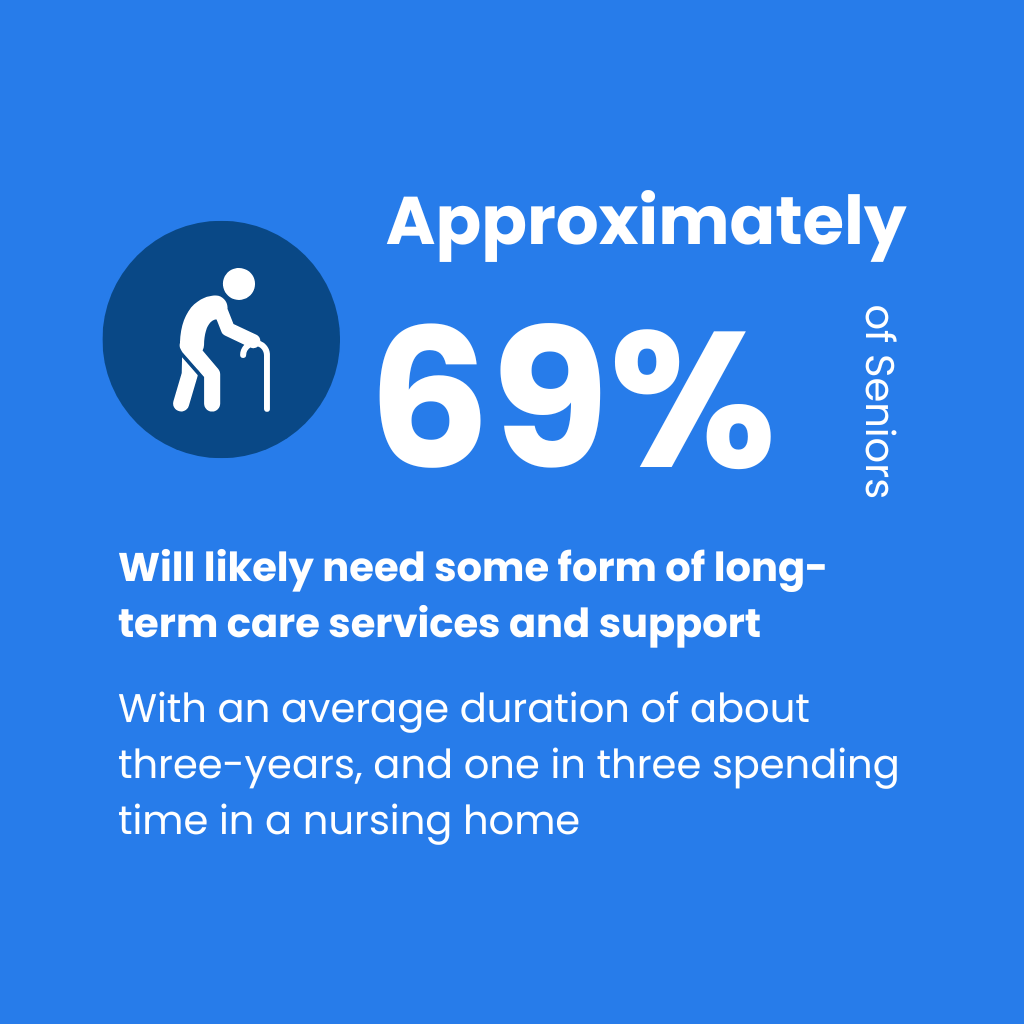

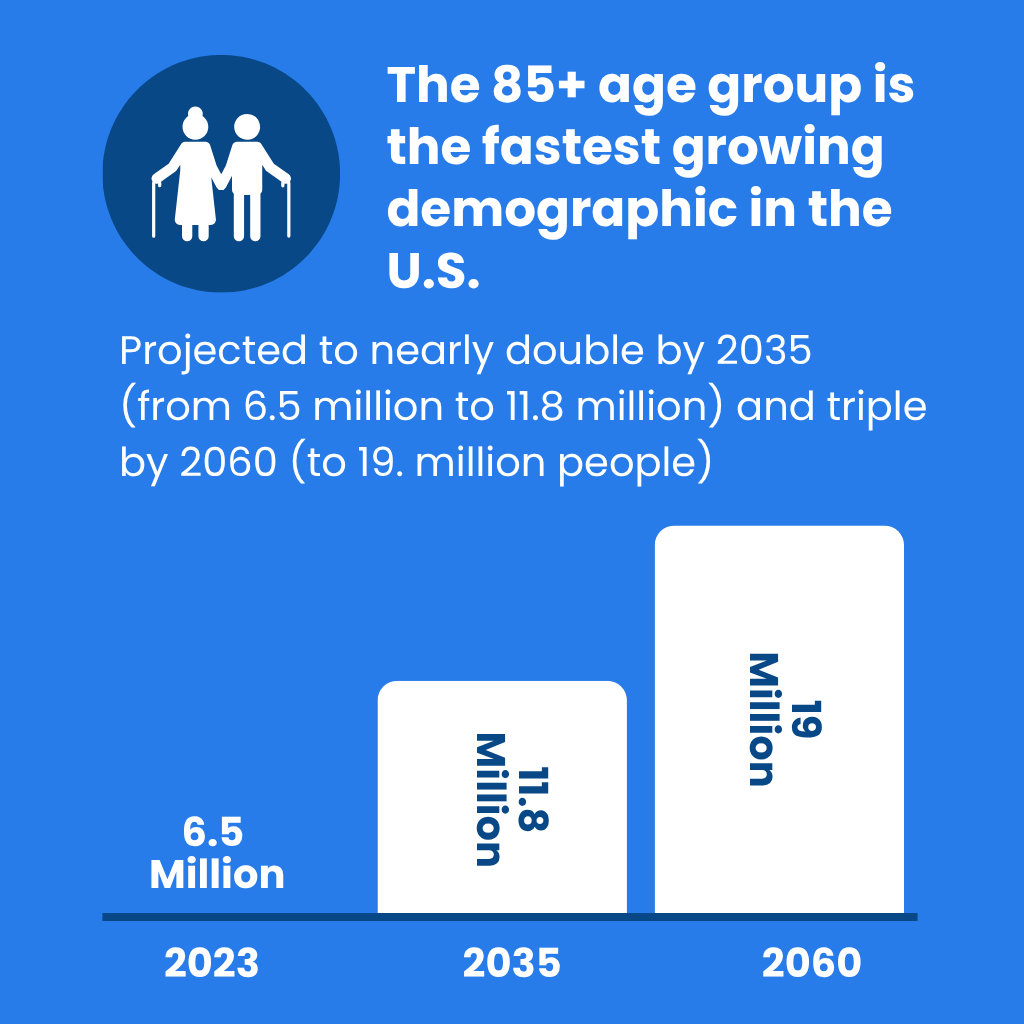

Every day, 10,000 Americans turn 65. One in three people retiring today will live into their 90s, and the fastest-growing age group in North America is over 85. Traditional retirement planning simply isn’t enough for clients facing decades of aging-related decisions.

Elder planning picks up where retirement planning stops—helping clients navigate healthcare, caregiving, family dynamics, diminished capacity, and legacy preservation. By mastering these skills, you not only safeguard your clients’ well-being but also secure your position as their most trusted advisor.

Differentiate Your Practice

Move beyond traditional financial planning to specialized expertise in the fastest-growing market segment.

Serve an Underserved Market

Develop deep skills in elder planning where few advisors have comprehensive training.

Be the Holistic Advisor

Build your reputation by addressing the full spectrum of aging concerns—financial, emotional, and practical.

Unlock New Revenue Streams

Create specialized service offerings with higher fees and longer client relationships.v

About the Program

The Elder Planning Specialist Program (EPS) A First-of-Its-Kind Certification for Financial Professionals

Created by renowned elder planning experts and jointly offered by Plan4Life, LLC and the Financial Planning Association, this 12-week online program equips forward-thinking advisors to better serve aging clients with confidence, care, and specialized expertise.

Traditional vs. Elder Planning

Traditional financial planning ends at retirement. Elder planning begins where retirement planning stops—addressing the realities of aging, healthcare, family dynamics, and legacy.

| Feature | Typical Financial Plan | Comprehensive Elder Plan / Aging Plan |

|---|---|---|

| Primary Scope | Primarily focused on wealth creation, accumulation of assets, retirement income, investment management, and mitigating taxes. | Holistic approach that integrates finances with physical, emotional, social, health, legal, housing, and caregiving needs. |

| Planning for Incapacity | Focuses on having a financial power of attorney in place to manage finances. | Includes detailed protocols for identifying and addressing diminished capacity, elder abuse, and financial exploitation. Often recommends engaging a Daily Money Manager and monitoring accounts via technology. |

| Long-Term Care (LTC) Planning | May assess the adequacy of resources for typical LTC (starting around age 45-50). Often assumes Medicare covers most costs, which is a common misunderstanding. | Requires a comprehensive LTC plan (not just insurance). Involves stress testing elder financial scenarios, exploring self-funding, LTC insurance, VA benefits, and Medicaid planning (as a last resort, requiring elder law attorney expertise). |

| Legal Documentation | Includes foundational estate documents like Wills, Durable Power of Attorney (DPOA), and Trusts, often focused on asset transfer upon death or incapacitation. | Ensures all legal documents are up-to-date and account for longevity care situations. Emphasizes Health Care Directives, HIPAA releases, Living Wills, and the need to appoint a highly trusted DPOA due to exploitation risk. |

| Legacy | Focuses on transferring tangible wealth (financial assets, property) through a legal will and trust. | Incorporates the transfer of intangible wealth through an Ethical Will (or Legacy Letter), sharing values, wisdom, life lessons, and providing context for financial decisions. |

| Key Tools & Deliverables | Financial forecasts, asset allocation statements, retirement projections. | Utilizes specialty tools like the "Grab-N-Go" binder (or Lifefolio) for organizing crucial legal/health information, a Care Matrix detailing care options/costs, and completing the Five Wishes advanced directive. |

| Key Risks Addressed | Addresses general financial risks, but the risk of long-term care is often perceived as the greatest threat to retirement income. | Addresses the three great financial risks that can derail plans: 1) need for long-term care, 2) loss of capacity/scams/exploitation, and 3) remarriage/late-in-life relationships. |

| Housing Strategy | May briefly discuss real estate assets. | Creates definitive plans regarding housing stability, safety, accessibility, aging in place pros/cons (high cost of care, safety issues). Includes contingency plans for moving to Assisted Living or CCRCs. |

| Financial Advisor Role | Manager of investments and assets. | Serves as the "quarterback" or strategic coordinator who identifies gaps, uses a collaborative approach, and makes intentional referrals to specialized professionals (e.g., elder law attorneys, geriatric care managers). |

| Family Involvement | Family meetings, if held, are usually focused on financial history and asset disposition. | Requires intentional, facilitated family meetings to discuss healthcare, housing, care preferences, and end-of-life wishes transparently. Emphasizes establishing roles and responsibilities beforehand. |

| Core Objectives | Aims to ensure financial goals (e.g., retirement, college savings, purchasing assets) are met. | Aims to ensure the client maintains independence and quality of life while proactively preparing for longevity and inevitable changes. |

| Caregiving | Often neglects the severe toll of caregiving. | Assesses the caregiver's role and potential for burnout, noting that primary caregivers over age 66 have a 63% higher mortality rate. Plans for formal support like geriatric care managers and professional care providers. |

| Aging and Longevity Focus | Longevity literacy is closely related to retirement readiness. Assumes financial management remains unchanged unless moving to assisted living. | Focuses on the "when" of aging, not just "if". Assesses the client’s understanding of physical, emotional, and social changes that come with aging. Addresses specialized issues like Age 85 considerations. |

Is This Program Right For You?

This program is designed for financial professionals who want to stay ahead of client needs in a rapidly aging society. It’s a fit if:

What You’ll Learn

Week 1: Understanding the Aging Process and the Caregiver’s Role

The impact of aging on financial planning

Physical and cognitive changes affecting decision-making

Supporting clients in caregiver roles

Week 2: Diversity and Aging and Insights into Retirees 85+

Cultural competence in elder planning

Research-based insights on the oldest Americans

Addressing diverse family structures and values

Week 3: Legal Issues of Aging

Essential legal documents beyond basic estate planning

Protecting vulnerable clients from exploitation

Elder law vs. estate planning distinctions

Week 4: Approaches to Planning for Extended or Long-term Care

Funding options for care needs

Navigating the care continuum

Insurance strategies and Medicaid planning

Week 5: Social Security and Medicare Planning

Advanced optimization strategies

Healthcare cost management

Supplement insurance navigation

Week 6: Diminished Capacity, Elder Abuse, End-of-Life Plans

Recognizing warning signs of decline

Implementing protective measures

Advanced directive planning

Week 7: Structuring and Conducting the Family Meeting / Ethical Will / Legacy Letter

Facilitating crucial conversations

Managing multi-generational dynamics

Documenting non-financial legacies

Week 8: Developing a Marketing Plan

Positioning your elder planning expertise

Reaching your target audience

Building referral relationships with healthcare professionals

Week 9: Building an Elder Planning Team

Creating a professional network

Coordinating multidisciplinary services

Communication protocols with healthcare providers

Week 10: Review Final Assignment

Case study analysis and discussion

Peer collaboration and feedback

Final project preparation

Week 11: Create Your Elder Plan

Developing comprehensive client deliverables

Elder Plan creation and customization

Implementation strategies

Week 12: Present Your Elder Plan

Student presentations and peer review

Faculty feedback and certification requirements

Program completion and next steps

Program Format Designed for Busy Professionals

Learning Methods

On-demand video presentations from subject matter experts

Live weekly discussions every Thursday at 1:00 PM MT (recordings available)

Interactive assessments to reinforce learning

Email access to presenters throughout each module

Supplemental reading to deepen knowledge

Time Commitment

3-4 hours per week of coursework

1 hour weekly live discussion

Self-paced video consumption

Flexible scheduling for busy professionals

Hear From Our Graduates

Discover the impact our graduates are making—in their practices and in their clients’ lives.

Taught by Industry Experts

Learn from Respected Industry Experts

Our instructors include leaders in elder law, financial planning, social work, and caregiving—bringing diverse, real-world experience to help you serve aging clients with confidence.

{kind=link}

Be the Advisor Aging Clients Can Rely On

Join the Elder Planning Specialist Program and lead with empathy, insight, and credibility.

Got questions? Well, we’ve got answers

A reliable internet connection, a computer with video capability, and the ability to access an online learning platform are required.

Yes, all live sessions are recorded and available for viewing within 24 hours.

Yes, graduates are encouraged to participate in the Pioneer Mastermind, a subscription-based group designed for implementing the learned concepts, and instructors offer ongoing consultation opportunities.

This is an intensive 12-week certification program designed to provide a comprehensive understanding of late-in-life planning and care. It focuses on how financial advisors can address the complex needs of aging clients and their family caregivers. The program goes beyond traditional financial considerations, integrating healthcare, legal, housing, and caregiving needs into a holistic elder planning framework. It is education-based and does not promote any specific product sales.

This program is specifically designed for financial advisors who are currently working with or intend to specialize in the elder demographic and their adult family caregivers (typically the 40+ age group). It is also highly beneficial for advisors who have aging parents and wish to apply the learnings to their personal family situations. The program helps advisors differentiate their services and provide truly comprehensive financial planning.

The program offers a broad curriculum, including:

- Understanding the aging process and the caregiver’s role, highlighting the critical need for elder planning due to families often making decisions during crises.

- Diversity and aging, emphasizing cultural competence in financial planning, and specific considerations for communities like LGBTQ+ older adults.

- Crucial aspects of elder law, covering the three great risks to financial plans: long-term care needs, loss of capacity (leading to financial exploitation and scams), and issues arising from remarriage or new late-in-life relationships.

- The evolving long-term care landscape, driven by demographics and longevity (e.g., the “sandwich generation” and “solo agers”), and practical strategies for financial professionals to address it.

- Detailed Medicare and Social Security planning, including their complexities, costs, claiming strategies, and the importance of proactive, individualized planning.

- End-of-life planning and legacy building, with a focus on Advanced Care Planning using the “Five Wishes” advanced directive and the creation of ethical wills.

- Strategies for managing and protecting clients facing diminished mental capacity and elder financial abuse.

- Guidance on how to organize and run successful family meetings for clients, covering legal, healthcare, legacy, and financial aspects.

- Strategies for growing an advisory business by specializing in the elder demographic, including effective self-marketing and building a collaborative professional team.

The program is delivered over 12 weeks. Each week typically includes two on-demand lectures. Students participate in graded discussions, and the program culminates in a final assignment. Week 11 is allocated as an off-week for students to work on their final assignment, and Week 12 features live sessions where students present their elder plans to the class.

The final assignment requires students to create and present a comprehensive elder plan for a client, which can be either fictitious or real (with names changed for privacy). The plan should reflect the entirety of the course learnings, assessing the client’s circumstances and providing recommendations across various elder planning topics. These topics include the client’s understanding of the aging process, caregiver roles, diversity issues, crisis management (including a “grab-n-go binder”), transportation/mobility, medical care, quality of life, Age 85 specific concerns, family meetings, worst-case scenario planning, and end-of-life matters (such as Five Wishes, ethical wills, and funeral arrangements). The assignment also requires evaluating trade-offs, identifying a suitable elder planning team, and outlining an implementation plan with notes for monitoring and adjustments.

The program features a team of highly experienced instructors and experts with decades of practical experience. Key instructors include:

- Annalee Kruger: President of Care Right Incorporated, Co-founder of Plan for Life Now, and author of “The Invisible Patient,” with over 30 years of experience.

- Paul Malley: President of the National Nonprofit Organization “Aging With Dignity”.

- Harry Margolis: An estate planning and elder law attorney with over 30 years of experience, author, and founder of multiple legal resource websites.

- Marcia Mantell: A retirement business consultant specializing in Medicare and Social Security planning.

- Susan Turnbull: A personal legacy advisor specializing in ethical wills.

- Terry Bradford Crane: A Certified Financial Planning Practitioner and financial literacy advocate, focusing on diversity and cultural competence in planning.

- Bob Mauterstock: Co-founder of Plan for Life Now, author, and expert in diminished capacity and family meetings.

The program equips financial advisors to:

- Offer a higher level of service by addressing the holistic needs of aging clients, moving beyond purely financial considerations.

- Deepen client relationships and generate referrals by providing tools and scripts for initiating and facilitating difficult but crucial conversations about aging, caregiving, and end-of-life wishes with clients and their families.

- Build a collaborative network of professionals (e.g., elder law attorneys, geriatric care managers, Medicare specialists, realtors), enabling them to act as a “quarterback” for their clients’ complex elder care needs.

- Utilize actionable marketing strategies specifically tailored for the elder demographic and their caregivers, including creating eBooks, establishing a strong social media presence, and networking with complementary professionals.

- Help preserve clients’ assets under management by proactively planning for long-term care needs and preventing caregiver burnout, which can have significant financial repercussions.

- Differentiate their practice from competitors by offering specialized expertise in elder planning.

The program offers unique insights into:

- The phenomenon of the “silver tsunami,” highlighting the demographic shift towards increased longevity and the rising prevalence of dementia among clients.

- The often overwhelming and critical role of family caregivers and the severe risks of caregiver burnout, including a 63% higher mortality rate for primary caregivers over 66.

- The importance of addressing the “when” of aging, not just “if,” encouraging early and proactive planning to avoid crisis-driven decisions.

- A detailed understanding of the three greatest risks that can derail seniors’ financial plans: long-term care needs, loss of capacity (leading to scams and financial exploitation), and issues arising from remarriage or new late-in-life relationships.

- Practical tools and resources such as the “Grab-and-Go Binder” for organizing crucial information, the “Care Matrix” for evaluating care options, and the “Five Wishes” document for advanced care planning.

This program aims to make financial advisors heroes to their clients by enabling them to provide truly holistic and comprehensive support through every stage of aging.